Why use a Mortgage Broker

Having a Kahuna Financial mortgage broker negotiate finance on your behalf is the smart way to save you time, stress and money.

Buying a home

We have access to hundreds of loans from a wide variety of lenders and will work with you to find the loan that suits your circumstances.

First Home Buyers

As a first home buyer, you may be eligible for a first home buyer grant.We can help you find out how much grant money you could receive.

Refinancing

The right refinanced loan could help you pay off your mortgage faster and for less, clear unhealthy debt or help you upgrade and add value your home

Investing in Property

It definitely pays to do your homework on the property market before you dive in, and we’re thrilled to be on board to help you when it comes to financing your decision.

Construction Loans

Most people cannot afford to pay for the cost of home construction up front, and getting a mortgage can be tricky. Kahuna Financial can help.

Kahuna Financial Management has been helping clients in Canberra and Sydney since 2016 with Bob and Ed helping customers achieve their lending goals since 2004. Our team of qualified and experienced mortgage brokers will guide and support you through every step of your journey.

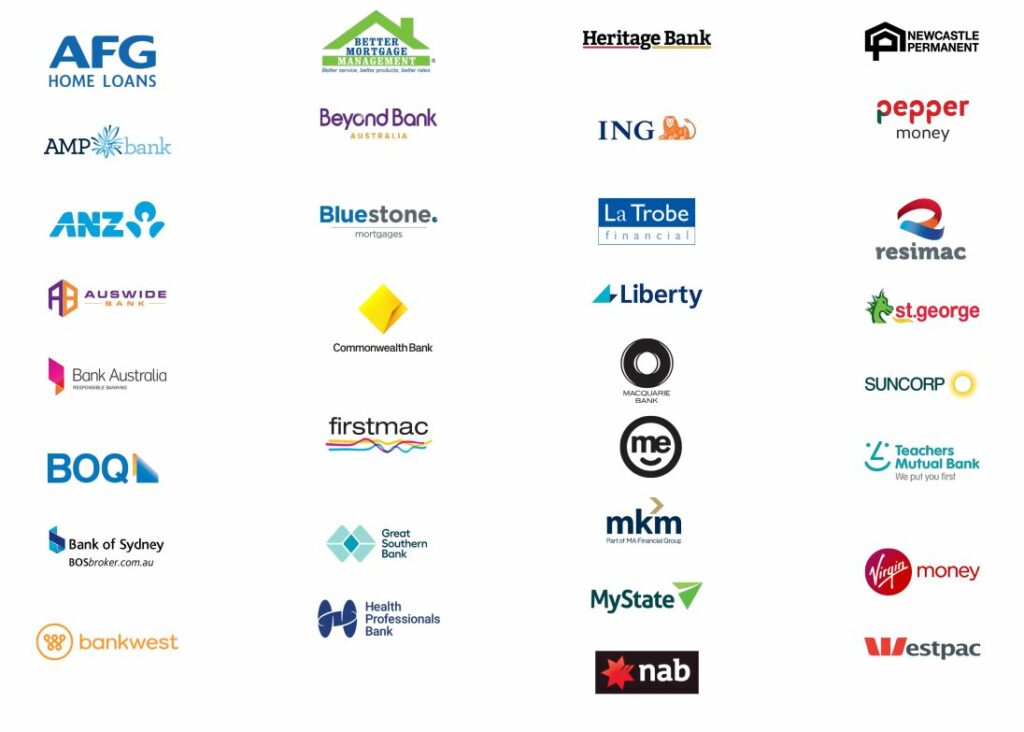

Being authorised accredited mortgage brokers provides transparency and the ability to work for you in your best interests. We have access to over 30 lenders to tailor a lending solution for your needs and circumstances.

Why Choose Us?

- Knowledge & Experience – Our mortgage brokers are highly qualified and have a breadth of knowledge and experience to focus on achieving the right lending outcome for you.

- Personal Service – Our focus on listening and understanding your situation, has enabled us to help our clients and run a business based on strong referrals.

- Transparency – As authorised accredited mortgage brokers, we act in your best interests to locate the most suitable solution across our lender panel. We are paid similar commissions from our lender panel and fully disclose this to you.

- Ease & Convenience – in working with us, we have access to many lending solutions that make the process easier and convenient for you.

- Keep you on track – we will stay in touch with you throughout the loan process and after settlement.

- Ongoing Support – Even after your loan has settled, we are here to support and answer any questions you have. Things change in our lives, and we are here to help into the future

- Licenced and Authorised – As authorised and accredited mortgage brokers we are members and representatives of;

- MFAA – Mortgage & Finance Association of Australia

- AFCA – Australian Financial Complaints Authority

- AFG – Australian Finance Group

The gift of giving this Christmas

Christmas is a time when we come together to celebrate with our family and friends. And, for those who haven’t…

Positives and negatives of gearing

Negatively gearing an investment property is viewed by many Australians as a tax effective way to get ahead. According to…

Are your insurance needs covered?

The start of a new year is always a good time to check whether your insurance policies are still serving…

Super changes add flexibility

Just when you thought you had a grip on the superannuation rules, they change again. This time though, the changes…

Cash is king in a crisis

Most of us understand the importance of saving for a rainy day, but sometimes it takes a crisis like the…

Getting retirement plans back on track

After a year when even the best laid plans have been put on hold due to COVID-19, people who were…